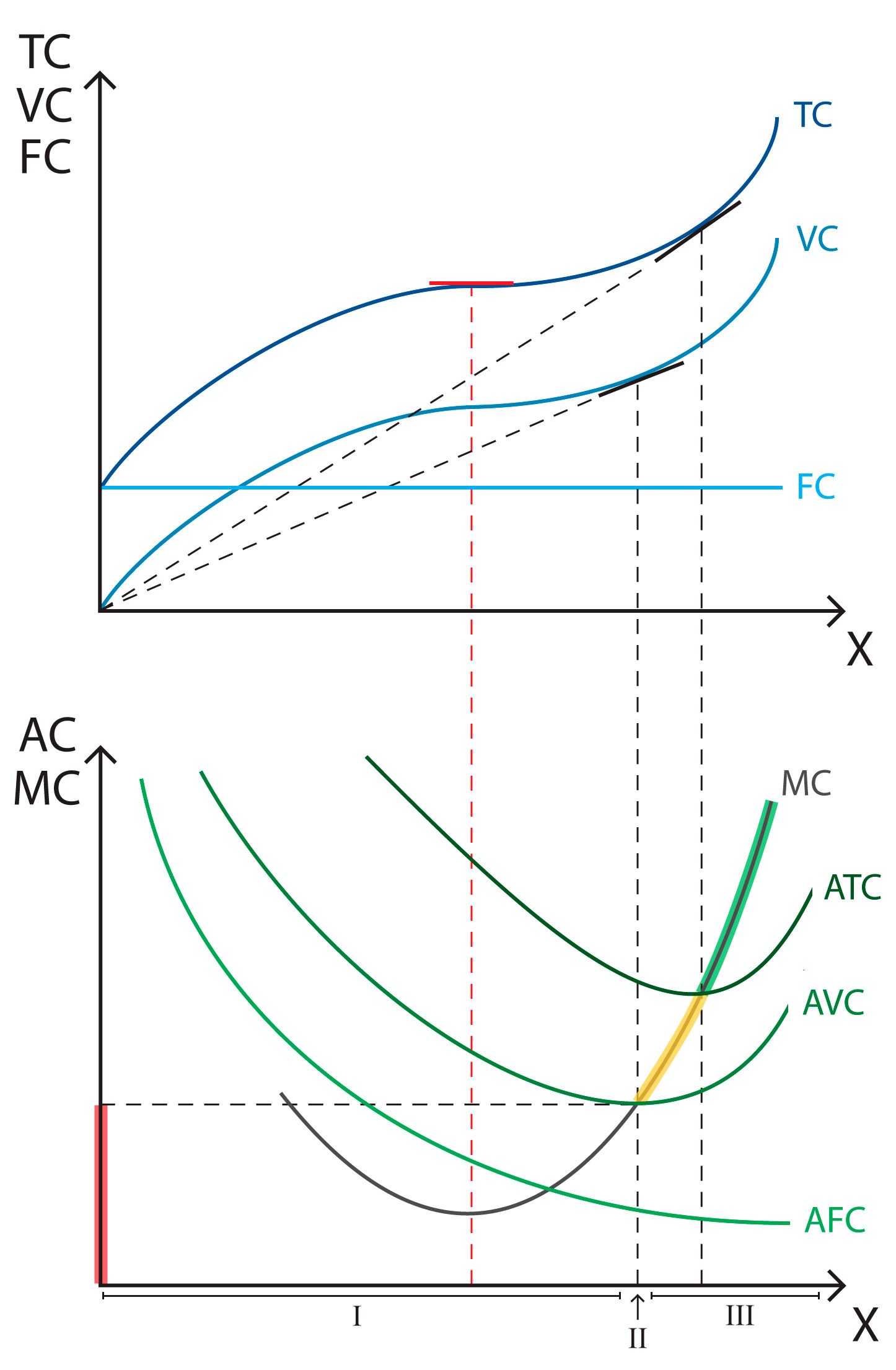

Average costs are those associated to one unit of production. Costs per unit grow quicker as production increases, so we find the arithmetic average as the sum of costs divided by the sum of production:

| Av. fixed costs: | Av. variable costs: | Av. total costs: | ||

Marginal costs are a very important concept in Economics because they show costs at a very specific point in time: they show the cost associated with producing one additional unit at any given production level.

They are the partial derivative of total or variable costs. This is an important point: because the partial derivative as respects quantity is zero for fixed costs (as these are independent of production levels), the partial derivative of variable and total costs is the same. Marginal costs, as any derivative, are tangent to total and variable cost curves at each point.

![]()