The theory of consumer choice under situations of risk and uncertainty belongs to the field of microeconomics. Risk and uncertainty are sometimes interchangeable terms but their meaning is easily misunderstood. Frank Knight in his “Risk, Uncertainty and Profit” 1921, treated this subject and posed a fundamental distinction between the two, formulating the definition that, ever since, became the most widely used.

In a situation that involves risk the outcome is unknown, but the distribution or the probability of its occurrence is known. These probabilities can either be objectively specified or subjectively, meaning that the agents will form their expectations regarding these probabilities. Sometimes it is said that risk is a known-unknown while uncertainty an unknown-unknown, since in the latter agents cannot (or will not) assign probabilities to each outcome.

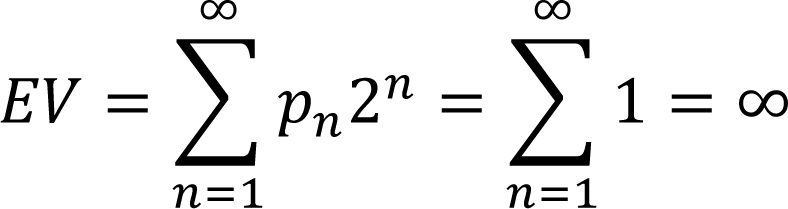

Consumer choice under risk is usually analysed using the expected utility theory approach, while uncertainty is studied mainly in game theory. However, although different models have been developed for both situations, risk situations, are the ones that have received the most attention and economists have concentrated on the analysis of risk probably due to its well-defined probability distribution in comparison with the random variables that uncertainty involves.

It must be mentioned that Daniel Kahneman co-authored with Amos Tversky in 1979 the paper “Prospect Theory: An Analysis of Decision under risk”, which drastically changed the way economists analyse decisions under risk. Their analysis is known as prospect theory, which studies the results from a series of empirical data and has very different conclusions from those drawn by expected utility theory.