Under a no separate legal tender regime, a country uses another one’s currency and thus gives away its capacity of using monetary policies. As stated by the IMF, under an exchange arrangement with no separate legal tender, “the currency of another country circulates as the sole legal tender, or the member belongs to a monetary or currency union in which the same legal tender is shared by the members of the union”. Following this definition, we could include every country in the Eurozone. However, since in that case a new central governing entity, the European Central Bank, was created, it is considered as a pure monetary union.

The most widely used example of an exchange arrangement with no separate legal tender is a formal dollarization. In this case, the country adopts the dollar as its currency. The most common examples are the cases of Ecuador, Panama and El Salvador. El Salvador is a rare case since dollars coexist with the former domestic currency, the colón. However, the printing of new colones is prohibited, so they will coexist with dollars until all colón notes wear out physically.

The main implication for a country to adopt an exchange arrangement with no separate legal tender is that it completely surrenders its control over monetary policy. Therefore, usually this regime is adopted by governments that are considered as non-reliable, substituting their currency in favour of a currency of another country considered to be stable and with an effective monetary policy.

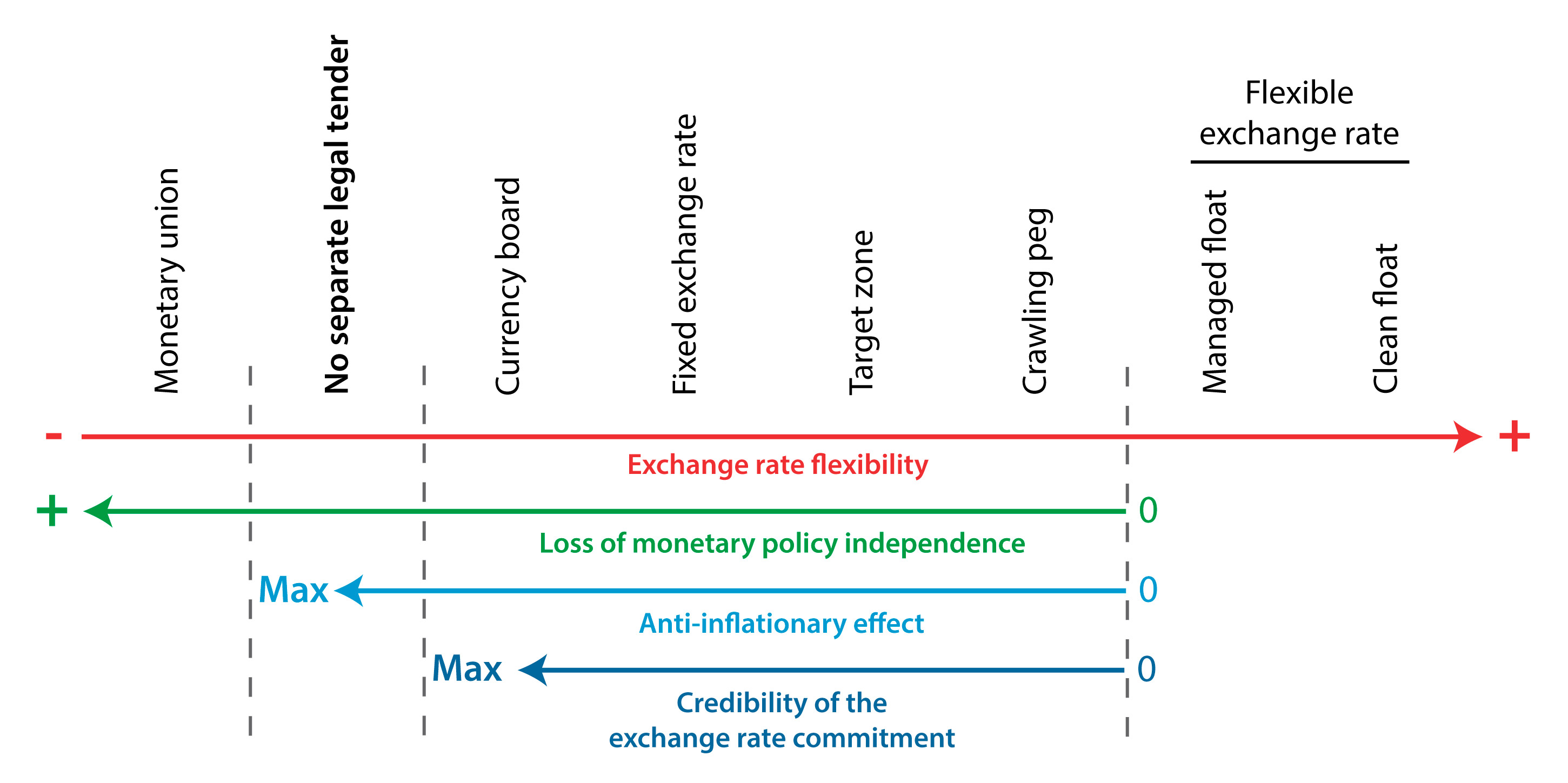

The following figure shows the different regimes according to four different variables: exchange rate flexibility, loss of monetary policy independence, anti-inflation effect and credibility of the exchange rate commitment: