Summary

In this LP we learn a bit more about risk, but also about uncertainty. We start by seeing again how risk is analysed using Morgenstern and von Neumann’s expected utility theory. We also learn about alternative approaches, such as the Friedman-Savage and Markowitz perspectives, but especially Daniel Kahneman’s prospect theory. We end our study of risk and uncertainty by learning how game theory can help when analysing uncertainty.Oskar Morgenstern and John von Neumann’s expected utility theory, which analyses individuals’ risk aversion, proves that different individuals have different perspective towards risk. Risk averse individuals have, by definition, a greater preference to avoid risky situations than risk-loving individuals and, to this end, they will be willing to pay an extra amount of money in order to mitigate (or eliminate) the bad consequences of such a risk.

Expected utility theory holds that the demand for insurance can be translated as a demand for certainty. Individuals will prefer to buy insurance in order to assure a certain amount of money (or to have a guarantee of lower losses), instead of its actuarial equivalent uncertain one. The insurance market allows agents to cover themselves against risk. Insurance companies take advantage of risk averse individuals to charge an extra surcharge to pay costs which are not covered by the premium. How individuals perceive insurances depends on their prices, and on the individuals’ preferences and budget constrain. A risk averse individual may be willing to assure against a potential loss, but will pay only up to a certain price for this insurance: if the price exceeds this amount he will not acquire the insurance.

We will use an analytical example for a better understanding:

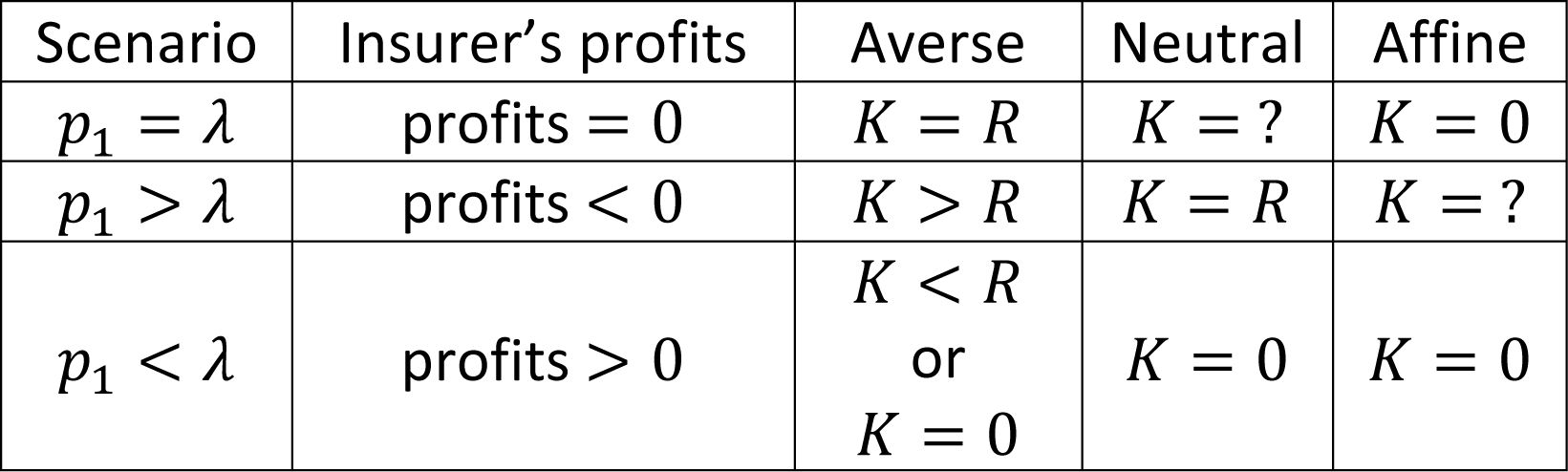

Imagine an individual with an initial wealth of W0 who faces the possibility of getting robbed an amount of R. He or she has the option of insuring an amount of K for a risk premium of λK. There are two possible scenarios:

S1, with a probability of happening p1: there is indeed a robbery, the individual loses R;

S2, with a probability of happening p2: there is no robbery.

We’ll have a budget constraint, in terms of wealth, such as:

![]()

![]()

The optimum point, given the budget constraint and being MU the marginal utility, is:

![]()