Summary

Everyone has to make decisions, but it is not always clear to us what outcomes can derive from these decisions. When this happens, we say we are making decisions in situations under risk or uncertainty. In this LP we learn about risk and uncertainty. We see how risk can be analysed by using expected utility instead of expected value, and how different kind of people will behave differently when facing risk.Risk and uncertainty:

Expected utility:

- St. Petersburg paradox

- Expected utility

- Expected utility theory

Risk aversion analysis:

The Saint Petersburg paradox, is a theoretical game used in economics, to represent a classical example were, by taking into account only the expected value as the only decision criterion, the decision maker will be misguided into an irrational decision. This paradox was presented and solved in Daniel Bernoulli’s “Commentarii Academiae Scientiarum Imperialis Petropolitanae” (translated as “Exposition of a new theory on the measurement of risk”), 1738, hence its name, St. Petersburg. He solved it by making the distinction between expected value and expected utility, as the latter uses weighted utility multiplied by probabilities, instead of using weighted outcomes. However, since then, alternative approaches have been used by different researches to answer this paradox.

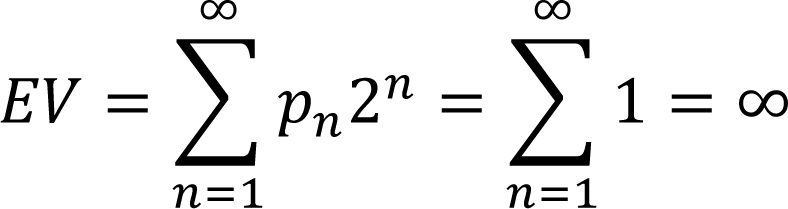

The key of the paradox is to determine the value someone would be willing to pay in order to play a lottery game that works as follows: a fair coin is tossed, if tail appears the player is paid $2 (in case the amount paid to play is $1), if not, the coin is tossed again, until tail appears, doubling the initial gain every time the coin is tossed. For example, for toss number 3 (n=3), the payoff would be 8 (2n) and the expected value, which here equals the payoff multiplied by the probability (here, 1).

The key of the paradox is to determine the value someone would be willing to pay in order to play a lottery game that works as follows: a fair coin is tossed, if tail appears the player is paid $2 (in case the amount paid to play is $1), if not, the coin is tossed again, until tail appears, doubling the initial gain every time the coin is tossed. For example, for toss number 3 (n=3), the payoff would be 8 (2n) and the expected value, which here equals the payoff multiplied by the probability (here, 1).

The probability that the first tail appears in the toss number n is equal to pn=1/2n, being 2n the payoff. Therefore, the expected value for n tosses would be:

If we use the expected value as the decision criterion, the player should be willing to pay $∞ in order to play. However, no rational individual would accept this. For Bernoulli, the answer relied in using the maximum expected utility instead of the maximum expected value:

![]()

Furthermore, Bernoulli stated that the utility will increase with the player’s wealth (since he or she would have more money to play), and decreasing marginal utility.

Bernoulli’s solution to the Saint Petersburg, although simple and concise, was later on greatly discussed and criticised by other economists. Knut Wicksell used it in order to develop interpersonal comparisons, while Francis Y. Edgeworth criticised its logarithmic utility function. Vilfredo Pareto replaced in his analysis of the paradox wealth by consumption, and Alfred Marshall replaced it with income.

Alfred Marshall’s analysis, present in his book “Principles of Economics”, 1890, is of great interest because, simply by replacing wealth by income, it changes the main conclusions and the solution of the paradox. Marshall explains how, when assuming decreasing marginal utility, no rational individual would play the game since losses would be greater than gains. As an example, shown in the adjacent figure, let’s say the probability of winning the game is equal to the probability of losing, hence ½. If a player loses, he or she will lose the money paid to play the game (x-1); if he or she wins, the player will win exactly the amount paid (x+1). Since area A is greater than B, because of the decreasing marginal utility, no rational player would play. As Alfred Marshall puts it:

Alfred Marshall’s analysis, present in his book “Principles of Economics”, 1890, is of great interest because, simply by replacing wealth by income, it changes the main conclusions and the solution of the paradox. Marshall explains how, when assuming decreasing marginal utility, no rational individual would play the game since losses would be greater than gains. As an example, shown in the adjacent figure, let’s say the probability of winning the game is equal to the probability of losing, hence ½. If a player loses, he or she will lose the money paid to play the game (x-1); if he or she wins, the player will win exactly the amount paid (x+1). Since area A is greater than B, because of the decreasing marginal utility, no rational player would play. As Alfred Marshall puts it:

“The clerk with £100 a-year will walk to business in a much heavier rain than the clerk with £300 a-year; for the cost of a ride by tram or omnibus measures a greater benefit to the poorer man than to the richer. If the poorer man spends the money, he will suffer more from the want of it afterwards than the richer would. The benefit that is measured in the poorer man’s mind by the cost is greater than that measured by it in the richer man’s mind.”