Summary

Traditionally, macroeconomics had been the realm of the Keynesians, whereas classical precepts had traditionally been applied to microeconomics and aggregated to have a shot at macro. NCM takes and applies this basis to develop a clear and coherent set of principles that aim to explain the major players, unemployment and inflation, from a fully neoclassical perspective.Main definitions and economists:

Unemployment and inflation:

- NCM’s Phillips curve

- Natural rate of unemployment

- Business cycles

- Cahuc’s adjustment cost

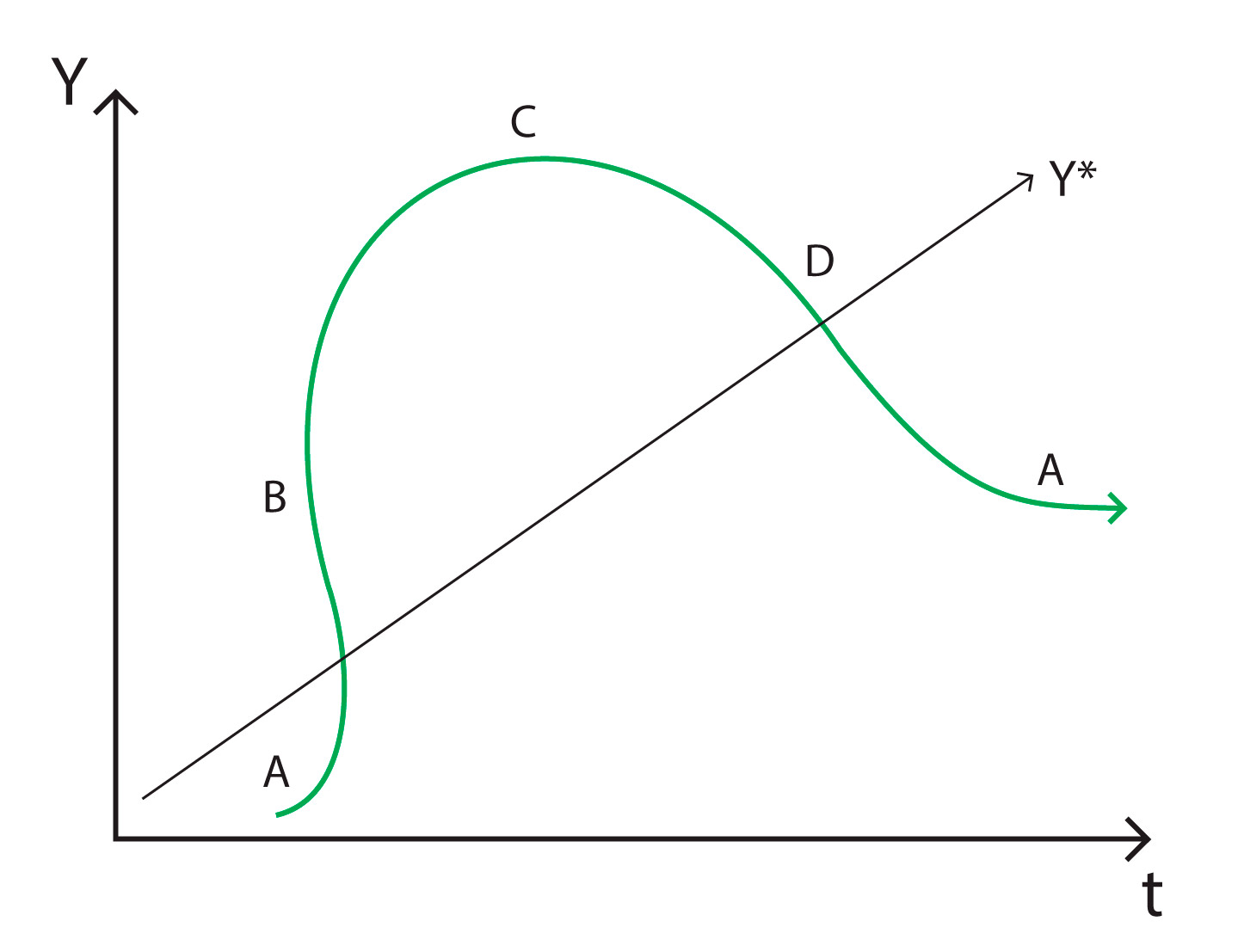

Business cycle, as Joseph Schumpeter saw it, is the economic activity fluctuation that occurs over time, and that comes from the succession of expansionary and contracting seasons. It is analysed comparing real GDP to potential GDP (Y*). There are a few common characteristics, which help differentiate cycles, such as its phases, the way it oscillates, the periodicity and a few stylized facts:

1. Phases:

Four phases can be distinguished, following Richard Lipsey’s classification:

-Trough or depression (A), characterized by a high rate of unemployment and low consumption levels in relation to its real capacity;

-Trough or depression (A), characterized by a high rate of unemployment and low consumption levels in relation to its real capacity;

-Expansion or recovery (B) of previous employment, income and consumption levels, that usually comes together with a rising in prices;

-Peak (C), distinguished by factors full use, high investment and shortage of labour, particularly for high-skilled jobs;

-Recession (D), demands fall causing unemployment and decreasing production levels.

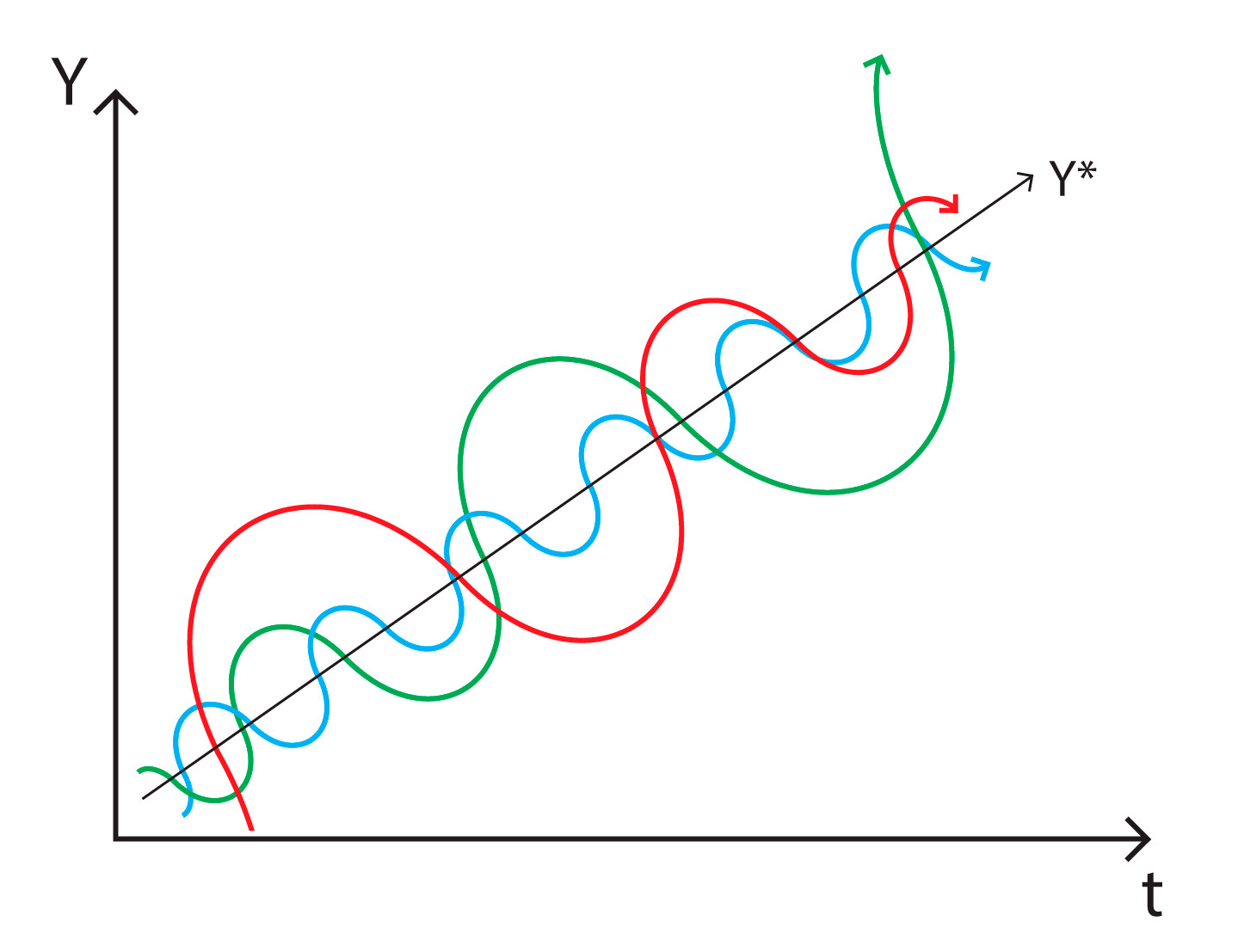

2. Oscillations:

|

-Oscillant cycles:

·regular oscillations (cyan); ·irregular, convergent oscillations (red); ·irregular, divergent oscillations (green). |

|

-Non-oscillant cycles:

·convergent (red); ·divergent (green). |

3. Periodicity:

Economic cycles have been classified depending in their periodicity. The most common are:

-Very short cycles, with duration of 30-40 months; also known as Kitchin cycles, whose studies saw in stock rotation the origin of these cycles;

-Short cycles, with duration of 7-11 years; also known as Juglar cycles, which origin is based on subsequent inventions;

-Long cycles with duration of 15-25 years; commonly known as Kuznets cycles, whose analysis placed the origin of cycles in demographic factors such as birth rates or migrations;

-Very long or Kondratiev cycle with duration of 50-60 years. This cycles originate with breakthroughs in capital goods, such as the steam engine or the Internet.

4. Stylized facts:

Both over time and between countries (a few of numerous reviewed by Robert Lucas in his article “Understanding Business Cycles”, 1977):

-There is positive correlation between variables, which helps smooth fluctuations;

-Co-movement between some variables:

·output fluctuates in the same direction in different sectors (although different amplitudes may apply);

·investment and consumption are clearly pro-cyclical: investment leads and is more volatile, consumption lags and is rather stable;

·income: real wages and profits are pro-cyclical;

·employment and labour force are also pro-cyclical.

-Expansions are usually longer than recessions.

Many papers and works have been written on business cycles and different points of view have taken form. Keynesian economics tries to deal with the economic fluctuation to minimize their impact. Business cycles are seen as a proof of market failure, and justify government intervention in order to assure the correct level of economic activity. Until the optimum level of employment has not been reached, the economy will not be readjusted. Depending on the cycle phase, expansionary or contractionary economic policies may be used.

New Classical Macroeconomics supporters have also dealt with economic cycles, and as a result the Real business cycle theory arises as an alternative view to Keynesian´s. Kydland and Prescott, and in general the Chicago School, are mostly related with the development of this theory. For them, cycles are explained by technological shocks. The fluctuations in the economy are seen to be produced by shifts in the supply curve, as a result of changes in productivity levels. These shocks can be caused by different factors: technology innovation, unusual weather conditions, changes in raw material prices, new policies and regulatory measures, etc. What is basic for these shocks to occur is an alteration in the effectiveness of either capital or labour factors, and therefore changing productivity. As a result in changes in the production quantity, the supply curve shifts, implying a new equilibrium point in the supply and demand model. Thus they believe that economy will reach its new equilibrium point, through the forces of demand and supply in itself, without the need for a government intervention. In fact from their view, government intervention will only worsen the situation.