When dealing with long run production, the main change from short run production is that we can vary the levels of fixed inputs we use (capital, K), as well as variable inputs (labour, L). Our levels of production will be determined by our returns to scale. It’s worth introducing here the concept homogenous functions. A function is considered homogenous if, when we have a multiplier, λ:

![]()

That is, we can reduce a production function to its common multiples multiplied by the original function. This is important to returns to scale because it will determine by how much variations in the levels of the input factors we use will affect the total level of production. Also, an homothetic production function is a function whose marginal rate of technical substitution is homogeneous of degree zero.

All this becomes very important to get the balance right between levels of capital, levels of labour, and total production. We can measure the elasticity of these returns to scale in the following way:

![]()

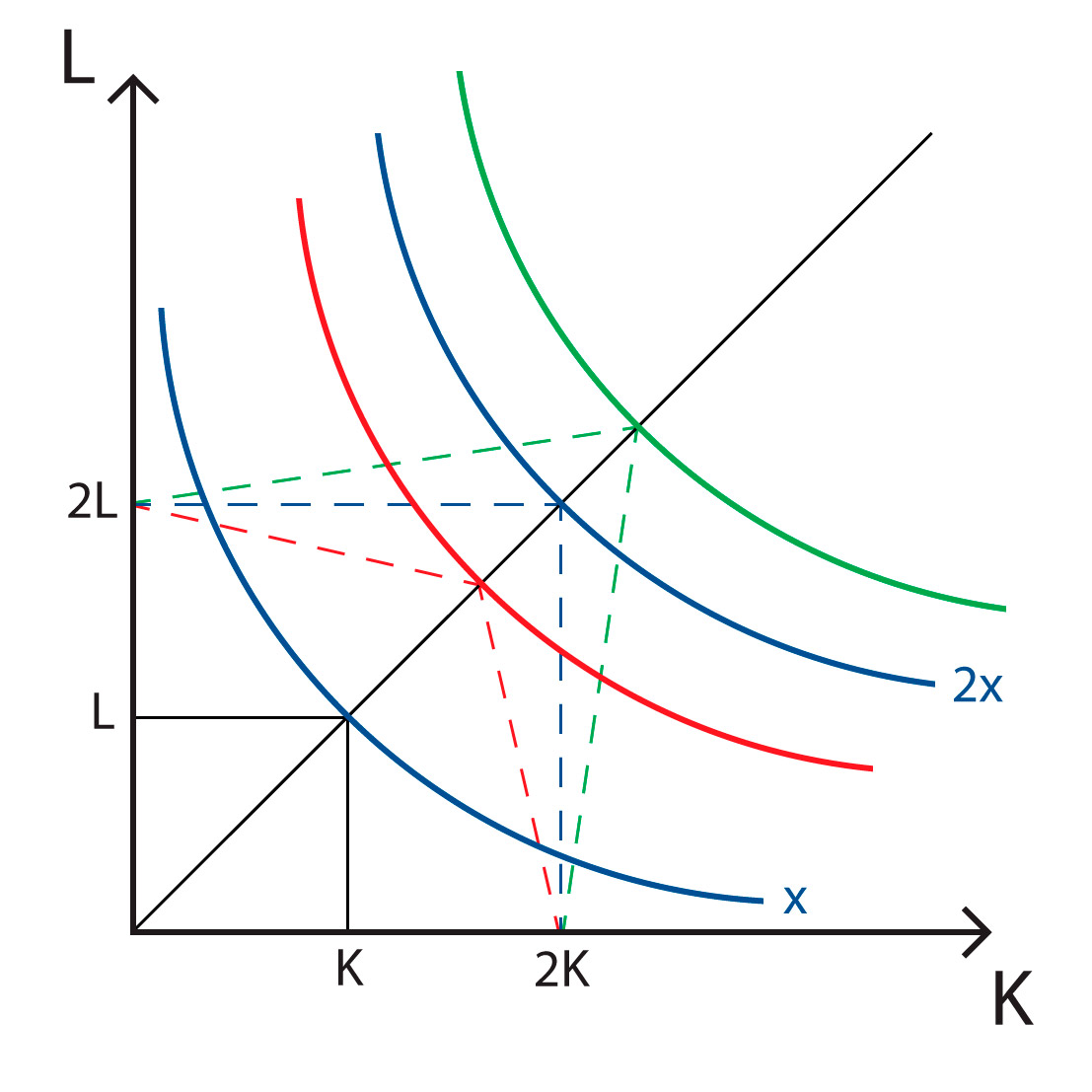

That is, the sum of the partial derivatives of production with regards to each factors multiplied by the proportion each input makes up of the whole. Graphically:

If µ is greater than one, we say that we have positive returns to scale (green). The more we produce, the less our costs will be per unit. If it is between one and zero, we have constant returns to scale (blue), and if it is negative, we will have negative returns to scale (red). When dealing with Cobb-Douglas functions, we can also determine which returns of scale are present, since α+β=µ.

All this will determine the average size of a business in the sector. Positive returns to scale, the most common scenario, will naturally attract a concentration of very large businesses, as is often the case in industrial, capital intensive sectors. Getting it right is crucial for another reason: in the long term, market equilibrium will determine that the total production of a certain good will be such to eliminate economic profits.