The Chamberlin´s model analyses and explains the short and long run equilibriums that occur under monopolistic competition, a market structure consisting of multiple producers acting as monopolists even though the market as a whole resembles a perfectly competitive one. The economist Edward H. Chamberlin gives name to this model, which he developed in his book “Theory of Monopolistic Competition”, 1933.

Assumptions

Chamberlin made a set of assumptions that were necessary for this market to perform properly. These assumptions include:

The existence of a set of products that the consumers perceive to be close substitutes. The crossed elasticity of these products is high but never infinite.

Each firm monopolises a product, although it shares the market with the rest of the industry.

There are a great number of firms in the market.

No entry or exit barriers to the market.

Full mobility of factors.

There is some degree of agent myopia in the sense that they do not learn from past errors.

Perceived vs actual demand

Chamberlin introduced in his model a distinction between perceived and effective demand curves. On the one hand, perceived demand, d in the adjacent figure, is the demand the firm is planning to supply or, in other words, how the firm believes customers will act to respect of its product. On the other hand, effective demand, D, is the way in which the market will act, in other words, how customers will act based on their perceptions on the market. However, consumers will always choose the best price and the greatest possible quantity, hence choosing always to be on what is called actual demand (green).

Chamberlin introduced in his model a distinction between perceived and effective demand curves. On the one hand, perceived demand, d in the adjacent figure, is the demand the firm is planning to supply or, in other words, how the firm believes customers will act to respect of its product. On the other hand, effective demand, D, is the way in which the market will act, in other words, how customers will act based on their perceptions on the market. However, consumers will always choose the best price and the greatest possible quantity, hence choosing always to be on what is called actual demand (green).

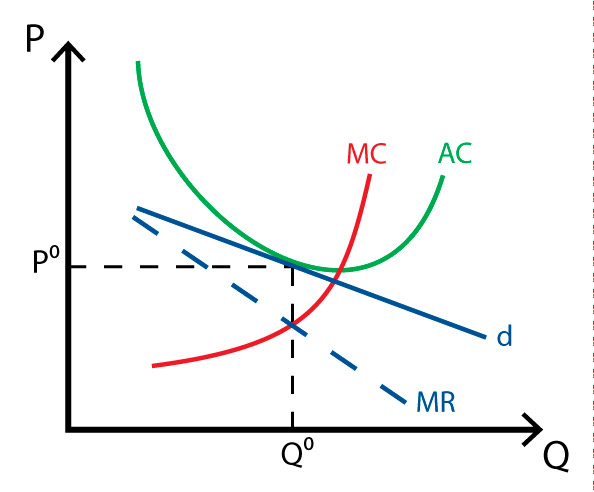

Equilibrium in the short-run

In the short-run, as shown in the second figure, each firm will act as a monopolist in its market. Given their demand and cost curves they will maximize profits by producing the level of output at which marginal cost equals marginal revenue. Whether they make profits or not will depend on the cost structure. In our example, there are no profits.

Equilibrium in the long-run

In the long run, the cost structure of the firm varies, allowing it to lower its prices in order to attract more customers. Lets start analysing the equilibrium in the long run considering the firm is in this situation of equilibrium (A), and because of its profits, it has no incentives for changing its price. However, the extraordinary profits that the firm is making will attract new competitors to the market. Although aggregate demand in the market is maintained, the entrance of new firms will translate into a fall of the effective demand of the firm. This drop in the demand of the firm is illustrated by the shift of the demand curve to the left, from D to Dˈ and a new equilibrium point will be reached at B.

However the firm will want to recover its previous profits levels and will therefore lower its price seeking to attract customers. The rest of firms will follow the same strategy so no customers are lost, and therefore the changes in its competitors and own strategies will change the perceived demand of the firm, from d to d’. A new equilibrium will be reached at C but this time firms will be incurring in losses, as price will be below average cost. This loss of profits will cause the exit of firms from the market, displacing effective demand rightwards and perceived demand downwards, as each firm that remains in the market will increase their individual demand. This process will be repeated until the equilibrium point is reached, from D to D*. At this equilibrium point, E*, the demand curve will be tangent to average cost in the long-run and price set at this level. Profits will be equal to zero and hence no entry or exit of firms will occur.

Main conclusions

Chamberlin’s monopolistic competition model analyses a whole new market structure, apart from the classic monopoly and perfect competition. It demonstrates that in a market the number of firms can be irrelevant, and perfectly competitive results can be reached. In fact, in terms of welfare and product differentiation, monopolistic competition is desirable.

It’s worth mentioning that these results are similar to those of William Baumol’s contestable markets, since the number of firms in the market does not necessarily determine how competitive it is. Also, the results are contrary to the results found in Bertrand’s duopoly model.